2015 China Outdoor Products Market Report

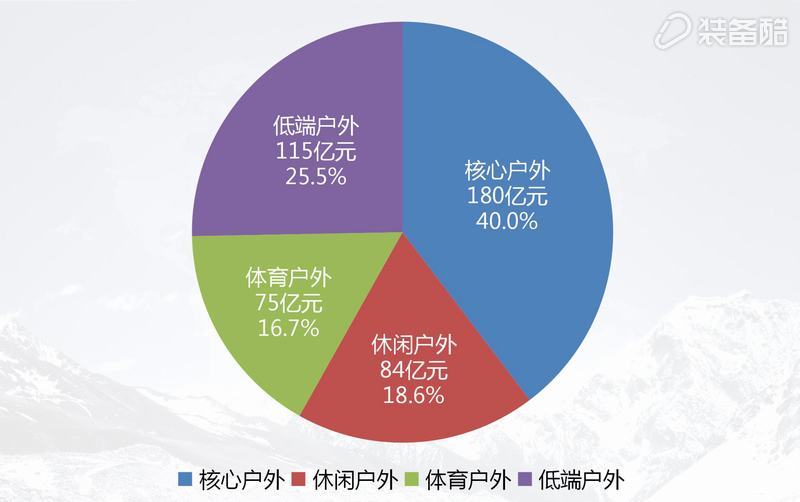

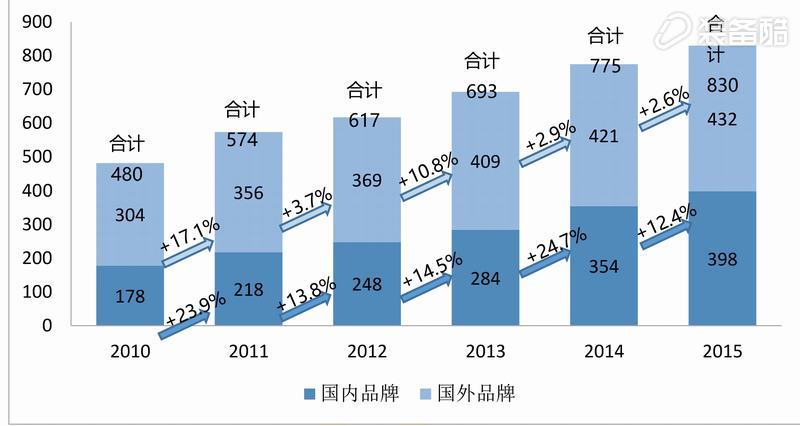

The COA China Outdoor Industry Report Conference was held at 10:30 am this morning at the Asia Outdoor Expo site, Nanjing International Expo Center, Hall 5A. The main contents of the report are as follows: In 2015, the overall outdoor market scale in China reached 45.4 billion yuan, an increase of 12.5% ​​over the previous year (Figure 1.1). In the past two years, the trend of the overall outdoor market in China has been that the growth rate of the core outdoor market has slowed down significantly and is still in the process of adjustment. The growth rate of the sports outdoor market is relatively fast. This is mainly due to the fact that after more than three years of adjustments in the sports brands, most sports brands have entered a new round of growth cycles since 2014; from the perspective of the 1Q16 results, major sports The brand is accelerating its growth. The prominent representatives are Nike and Adidas. The share of outdoor products of these two brands is also gradually increasing. Leisure outdoor market has not changed much. The share of the low-end outdoor market in the overall outdoor market has also changed little. However, it is worth noting that Decathlon's share in the low-end outdoor interior has increased rapidly. In the past two years, Decathlon has developed rapidly. By the end of 2015, there have been 158 retail stores in China, and the growth has not diminished. In 2015, the size of the core outdoor market reached 18 billion yuan, which represented an increase of 5.3% compared with RMB 17.1 billion in 2014. The growth rate has further declined from the previous year. Who brought this 5.3% growth in 2015? Different from the past 15 years, the big brands did not contribute much to the growth rate in 2015. According to the statistics of the top 50 brand sales, except for a few brands that grew by more than 10%, the increase of most brands was less than 5%. In 2015, some single leading brands and new online brands contributed a lot to market growth. In 2015, there were more than 50 new brands in the domestic outdoor product market, of which nearly 80% were online brands. At present, there are more than 100 online brands on the market. Of these, more than 10 have developed rapidly and are the main force for online sales growth. In the evolution of the past 20 years, during the period when street shops dominated, market sales were modest and it was a typical market cultivation period; after 2006, mall stores entered a period of rapid growth, and by 2013, the market share of channels exceeded 65%. ; Germany's outdoor brand "Dragon Claw" is the most prominent representative of the rapid growth opportunities to seize the mall channels. Since the brand entered the Chinese market, it has concentrated all its efforts on shopping mall channels, which has enabled the brand to develop rapidly. Both Le Fes and Colombia also rely mainly on shopping malls. In 2015, the percentage of street shops accounted for 21.7%, mall stores accounted for 62.9%, and online sales accounted for 15.4%. In the next five years, the market share of online sales will grow rapidly further. It is expected that the proportion of online sales will exceed 31% by 2020; the proportion of shopping malls and street shops will further decline; in street shops, small street shops will further reduce , The proportion of large street shops increased. At present, the process of channel changes continues to have a profound impact on the future market. In particular, the evolution of online marketing channels is far from over. Despite the poor stability of the online sales model, various new online sales models are still emerging, but the increasing share of online marketing channels is realistic. From this chart, we can clearly see the distribution of the domestic outdoor market. The western part of the country is the region with the most abundant outdoor resources in the mountains and is the destination for people to travel outdoors. However, the outdoor product market is mainly distributed in the economically developed regions in the east. We organize industry experts to identify 830 core outdoor brands out of more than 1,200 outdoor brands or self-proclaimed “outdoor brandsâ€. In 2015, the number of core outdoor market brands in the country continued to increase, which was 7% higher than the 775 in 2014. Among them, the number of domestic brands was 398, accounting for 47.95% of the total number of brands, and the growth rate was 12.4%; the number of foreign brands was 432, accounting for 52.05% of the total number of brands, and the growth rate was 2.6%. The growth rate of domestic brands is higher than the growth rate of foreign brands. Among the new domestic brands, 80% are so-called “online brands†that mainly rely on online sales. Knitted Type Pvc&rubber Air Hose

1.Using the newest formula technology of PVC & NBR and the most cutting-edge Korea forming technology.

2.The precise knit structure and reinforced by high tensile polyester yarn.

3.Light-weight, high pressure, low-temperature resistance, flexible, and excellent toughness at temperature -5℃ to +65℃ .

4.Good abrasion performance, chemical resistance, and expansion resistance. A long service life.

Knitted Hose,Chunky Yarn,Jersey Fabric,Stockinette Stitch YIYANG PLASTIC PRODUCTS CO., LTD , https://www.yiyang-hose.com

First, the market

1. Overview of the domestic outdoor product market in 2015 For most of the practitioners and companies in the outdoor industry, 2015 was a difficult year.

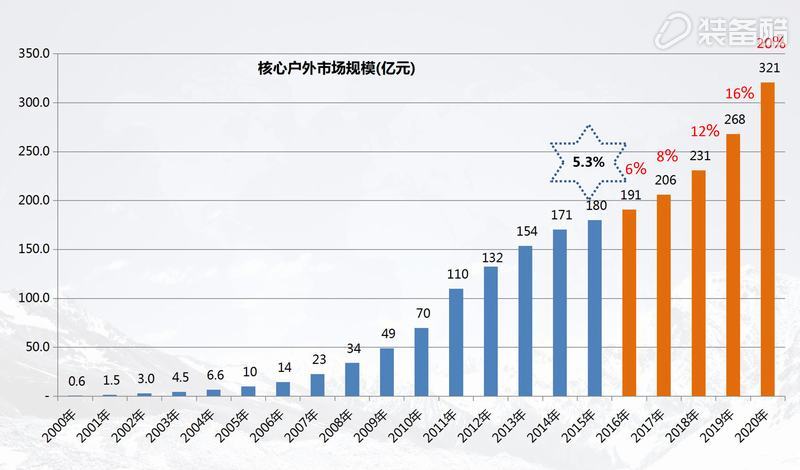

As an emerging sunrise industry, the outdoor supplies industry has started its development in the mid-1990s and has experienced rapid development for over 20 years. According to COA statistics, the compound annual growth rate of the domestic outdoor products industry from 2001 to 2010 exceeded 60% in 10 years; in 2011, the retail market scale exceeded 10 billion yuan for the first time, exceeded 15 billion yuan in 2013, and the market size reached 18 billion yuan in 2015.

Like all emerging industries, after the rapid development, ushering in the "adjustment period" is an inevitable process of industrial development. In 2013, the domestic market for core outdoor products increased by 16.7% over the previous year. The growth rate was below 20% for the first time. In 2014, it increased by 10.9% compared to 2013. In 2015, the growth rate was only 5.3% compared to 2014; the domestic outdoor products industry has experienced many years. After the rapid growth, it will enter the adjustment period from 2014.

In interviews with more than 50 companies, nearly half of the company's heads of staff talked about the most complex current market environment and competitive pressures faced by companies. To sum up, “In the context of profound changes in the country’s overall economic environment, there are issues that have arisen from the internal experience of the industry for more than two decades of high-speed growth and accumulation, and there are external forces in the industry who regard the outdoor industry as a sunrise industry. The entry into the market has intensified market competition. " There is a person in charge of the company figuratively metaphor: "The market's new brand speed is far higher than the market's growth."

"Adversity is heroic." In the interview, while we felt that the adjustment period brought pressure on the company, it is even more gratifying that we have seen great progress in Chinese domestic brands in the past two decades. Outdoors, as a typical foreign trade industry, is dominated by foreign brands at the beginning of the industry, and now has more than half of the local brand market share. A group of local leading brand enterprises regard this adjustment period as an opportunity period. We will firmly grasp the time window provided by the market adjustment period and profoundly examine ourselves “brand positioning and development strategies, exercise internal strengths, and enhance our self-development capabilities†and adopt a more mature attitude to welcome the arrival of a new round of growth cycles in outdoor industries.

2. The overall outdoor product market With the development of outdoor industries, more and more industry brands have begun to engage in the outdoor product industry. This situation has on the one hand enriched the connotation of the industry, and on the other, it has also blurred the industry to some extent. The extension.

We divide the outdoor product market into four components based on the degree of product fit with outdoor sports:

1) The core outdoor market is composed of professional outdoor brands. Professional outdoor brands are those brands and companies whose roots are in the outdoor industry and whose main revenue comes from the outdoor industry.

2) The sports outdoor market, which consists of sports brands with outdoor products, refers to the main line of products as traditional sports products, but some of its product lines already include outdoor products, but have not yet become the brand of its leading products. For example Adidas, Nike, Li Ning, Anta and so on.

3) The leisure outdoor market, which consists of fashion and leisure brands with outdoor products, refers to its main line products as fashion and leisure products, but some of its product lines already include outdoor products, but have not yet become the brand of its leading products. For example, LOTTO, JEEP, CAMEL ACTIVE, etc.

4) Low-end outdoor market consisting of low-end consumer market brands with outdoor products. For example, many outdoor brands are sold in supermarkets such as Quechua, Metro, and Walmart.

We divide the outdoor product market into four parts, which will help us to study the changes in the market and see the full picture of the outdoor market. In particular, for market investors, “there is a clear boundary definition, and statistical data have reference valueâ€.

3, the core outdoor market

2000-2015 Domestic Core Outdoor Market Scale (Figure 1.2)

In Figure 1.2, the growth rate for 2016-2020 is forecast data.

The "adjustment period" that began in 2014 is expected to last three to four years. Most brands will enter a new growth cycle from 2017. Therefore, our market expectation for the 2016-2020 five-year period is that in 2016 and 2017, it will still be a single-digit growth, with a growth rate of 2 digits in 2018 and 2019, and a growth rate of more than 20% in 2020.

Second, the channel

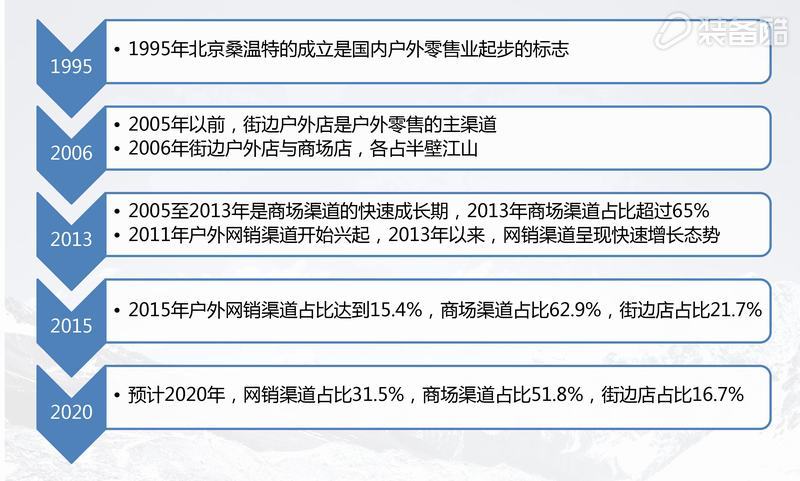

1, outdoor channel composition and evolution trends Outdoor supplies sales agencies including various levels of agents, distributors and so on. The focus of this report is on outdoor retail terminals, which mainly include: department store channels, professional outdoor stores (street stores), and online sales channels.

1996--2015 Schematic diagram of the evolution of sales channels in the core outdoor products market in China (Figure 3.1)

After 2006, shopping malls have become the main channel for outdoor footwear and clothing products. This situation is very different from that of European and American markets and has Chinese characteristics. In the consumer survey, it can be clearly seen that there are many consumers of outdoor products in China, and wearing outdoor clothing as a fashion is not associated with actual participation in outdoor sports. Such consumer groups are the main consumers of shopping mall channels.

In 2011, online sales began to rise, and after 2013, it has shown rapid growth. The Pathfinder is the first big brand whose online sales accounted for more than 30%; Bo Xihe is a typical representative of the rapid development of online brands in the past three years.

In the next few years, the share of online sales channels will continue to rise, further crowding out the street stores, including the market channel share. Although the share of street-side shops and shopping malls is declining, the demand for large-scale experiential stores is increasing, especially the demand for large street-side experiential stores. In 2015, the number of small street shops decreased significantly. At the same time, a large number of large-scale street-side shops were added. This phenomenon deserves attention.

2. Channel market share and trends

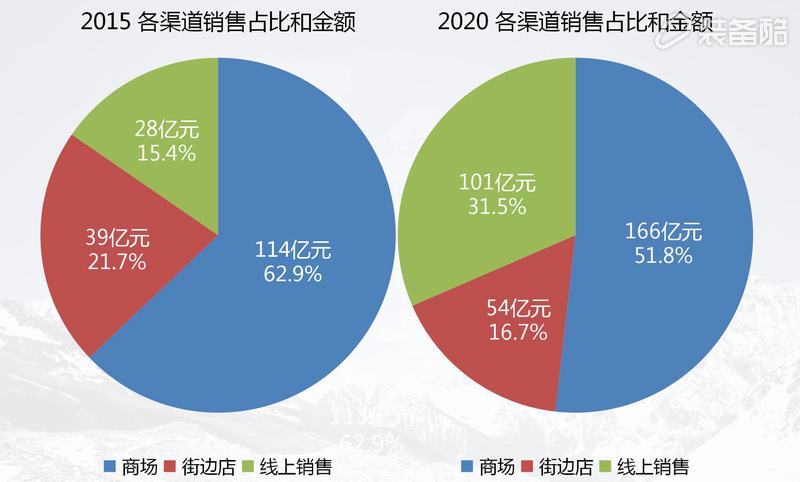

2015 Market Share of Various Sales Channels and Forecast of Channel Market Share in 2020 (Figure 3.3)

Special note: In the past three years, with the rapid growth of online channels, a large number of online products have emerged. Many online products are flaunted by outdoor banners and do not meet the criteria for core outdoor brands. To this end, the Branding Expert Group screened the existing online brands one by one, and classified most of the “online and outdoor brands†into casual outdoor brands. A considerable portion of the online brands listed in the core two years ago (2013/2014) were included. Also excluded. Based on this, we re-calculated the calculation model of online marketing channels in 2015.

We will further explain in the brand profile section that the definition of the brand, the division of the market, etc., also need to undergo a process of gradual standardization and improvement.

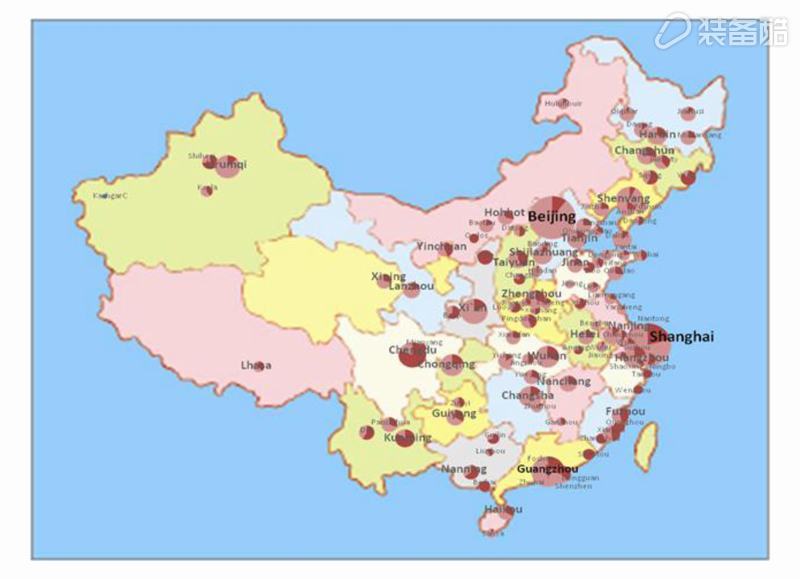

Domestic Outdoor Market and Physical Distribution in 2015 (Figure 3.2)

The north, especially the northeast region, is the main sales market for outdoor products and is closely related to climate factors.

Third, the brand profile

2010-2015 Trends in the number of core outdoor brands (Figure 2.1)

As can be seen from Figure 2.1, at present, the number of Chinese outdoor market brands continues to increase or decrease, but the growth rate has slowed down. Compared with the development history of the European and American outdoor markets, our common feature is that in the initial stage of market growth, new brands are generated in large numbers, and the number of brands is significantly reduced after the market matures.

The historical data of Korean outdoor brands is even more typical. From the 1980s to the 1990s, South Korea’s outdoor industry was rapidly growing. During the period, a large number of Korean brands were springing up, with a maximum of nearly 800. However, the brand that actually grew up is very limited.

From the perspective of the domestic outdoor market, the growth rate of offline brands has slowed down significantly; online brands will also grow for some time to come; but due to the lack of deep-rooted outdoor culture of online brands, some online brands will soon disappear. At present, the actual situation in the domestic outdoor market is that nearly 10% of brands actually exist in name only.

The proportion of sales to foreign brands' agents, the importance, sustainability, and feasibility of development are steadily declining. We believe this trend will continue. With the development of the domestic outdoor market, it is inevitable that the market's brand concentration will continue to rise. Although the pace of this process is unpredictable.

Finally, we must not lose sight of the capitalization of outdoor industries and the turbulent involvement of capital in outdoor industries. This includes two aspects. First, the capitalization of the industry itself is accelerating. In addition to the Pathfinder and Sanfu who have already achieved the IPO, several companies are on the road to IPO, and there are many brands and channel companies already The introduction of financial or strategic investors, thereby raising the level of capitalization of the entire industry. On the other hand, various investment institutions represented by private equity funds not only increase investment in brands and channels within the industry, but also have the tendency to purchase and operate brands, channels, clubs, and events directly. Given their financing and investment capabilities, it is likely to have a huge impact on the entire ecology of the industry.

In summary, 2015 was full of challenges and changes. In the future, we not only saw the potential and speed of gradual recovery, but also the possibility of numerous changes and the uncertainties brought about by these new changes. . How to seize opportunities, seize opportunities, and avoid traps in this huge uncertainty is both a challenge to existing companies in the industry and investors who plan to enter this field. It is also to realize the advantages of latecomers and through innovation. Realize the opportunity for rapid value-added business.

Survey Description This report was completed by a dedicated research team of China Outdoor Brand Alliance. In the report, while we insisted on the core outdoor market as the research focus, we also conducted in-depth research on non-core outdoor markets. We hope that through the study of market segments, through comparative analysis, readers will be able to grasp the full picture of the outdoor market more clearly. In particular, for market investors, “the boundaries are clearly defined and statistical data are more valuableâ€. We sincerely thank the members of the outdoor brand alliances for their support to the research team in terms of funds, products, and especially market data.

Data sources The core outdoor market sales data mainly comes from the interviews with the top 50 business executives or sales directors, as well as major regional distributors and retailers; due to the large number of sports brands listed, sports outdoor market data, mainly listed companies Based on the public data, the leisure outdoor market and the low-end outdoor market data are mainly based on domestic large-scale retail and retail textile industry market data and sales data of more than 20 well-known leisure brands.

The online sales data is mainly based on the public data of Tmall and Jingdong Mall.

Sources of physical retail terminal data: We selected 107 cities in 334 prefecture-level or above cities across the country, through more than 300 market investigators to make statistics on retail terminals at street stores and shopping malls, and established a database. The data base extrapolates the national data. Investigators are all from outdoor clubs or outdoor retail companies. They have formed a stable and cooperative relationship with the research team to ensure the dynamic update of the retail terminal database.

Brand Scope: A team of industry experts identified each of the more than 1,200 recognized or self-proclaimed “outdoor brands†one by one to determine the scope of core outdoor brands in 2015.

The research team's selection principles for various market data: We focus more on the industry market data accumulated by well-known brand enterprises over the years.

All statistics in this report do not include skiing, mountain biking, fishing, and hunting.

Information from: China Outdoor Brand Alliance COA Released